TAX REGIME SPECIFIC TO MUTUAL FUND INVESTORS IN INDIA FOR Financial Year 2022-23

I. TAX RATES FOR MUTUAL FUND INVESTORS

Tax & TDS are subject to applicable Surcharge and Health & Education Cess at the rate of 4%. Please see the Notes below

NOTES:

- Provided that the mutual fund units are held as capital assets.

- Tax to be deducted at source as per section 196A of the Income tax Act, 1961 (‘the Act’) [plus applicable surcharge, if any, and Health and Education Cess @ 4% on income-tax and surcharge].

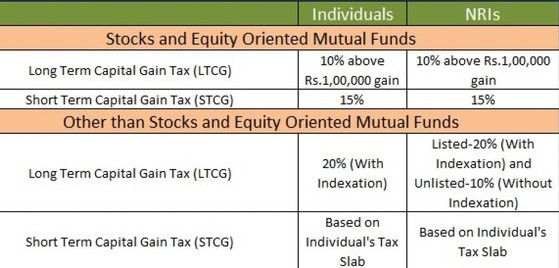

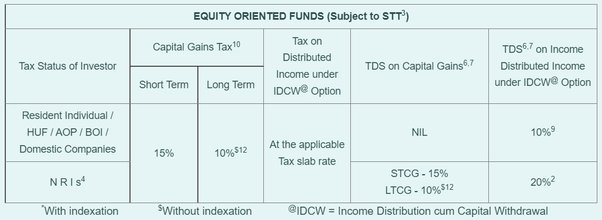

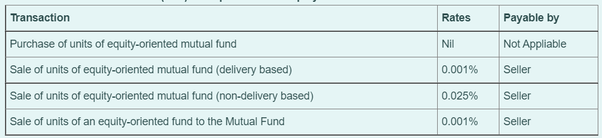

- Securities Transaction Tax (‘STT’) is applicable only in respect of sale of units of Equity-oriented funds (EOFs) on a recognised stock exchange and on repurchase (redemption) of units of EOFs by the mutual fund. STT in not applicable in respect of purchase/ sale/ redemption of units of other schemes (other than EOFs).

- Non-resident individuals (NRI) shall be entitled to be governed by provisions of the applicable Tax Treaty, which India has entered with the country of residence of the NRI, if that is more beneficial than the provisions of the Act , subject to certain conditions. As per section 90(4) of the Act, a non-resident shall not be entitled to claim treaty benefits, unless the non-resident obtains a Tax Residency Certificate of being a resident of home country. Furthermore, as per section 90(5) of the Act, non-resident is also required to provide such other documents and information, as prescribed by CBDT, as applicable.

- As per section 112 of the Act, long-term capital gains in case of NRIs would be taxable @ 10% on transfer of capital assets, being unlisted securities, computed without giving effect to first and second proviso to section 48 i.e., without taking benefit of foreign currency fluctuation and indexation benefit.

- Relaxation to NRIs from deduction of tax at higher rate (except income distributed by mutual fund) in the absence of Permanent Account Number (PAN) is subject to the NRI providing specified information and documents. As per provisions of Section 206AA of the Act, if there is default on the part of a NRI (entitled to receive redemption proceeds from the Mutual Fund on which tax is deductible under Chapter XVII of the Act) to provide its PAN, the tax shall be deducted at higher of the following rates: i) rates specified in relevant provisions of the Act; or ii) rate or rates in force; or iii) rate of 20%. However, the provisions of section 206AA of the Act shall not apply, if the requirements as stated in Rule 37BC of the Income-tax Rules, 1962, are met.

- Section 206AB of the Act provides for higher rate for TDS for the non-filers of income-tax return. The TDS rate in this section is higher of the followings rates: i) twice the rate specified in the relevant provision of the Act; or ii) twice the rate or rates in force; or iii) the rate of five per cent. However, the said provision does not apply to a non-resident who does not have a permanent establishment in India.

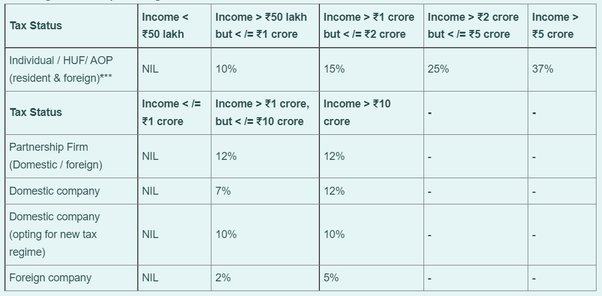

Surcharge Rate as a percentage of Income-tax

* The surcharge rate applicable to capital gains taxable under section 112A and 111A of the Act i.e. capital gains earned on sale of units of equity oriented mutual fund (which are subject to Securities Transaction Tax) is capped to 15%.

The Finance Bill, 2022 has further proposed to cap the surcharge rate on long-term capital gains taxable under section 112 of the Act to 15%.

**The Finance Bill, 2022 has proposed to rationalise the surcharge rates in the case of an association of persons consisting of only companies as its members as under —

- Income > ₹50 lakh but <= ₹1 crore 10%

- Income > ₹1 crore 15%

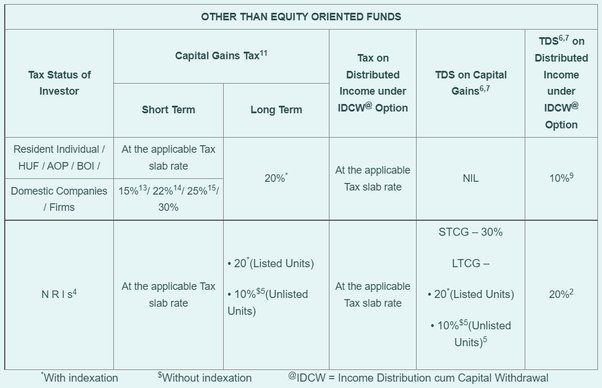

- There shall be no TDS deductible if IDCW income paid / credited in respect of units of a mutual fund is below ₹ 5,000 in a financial year.

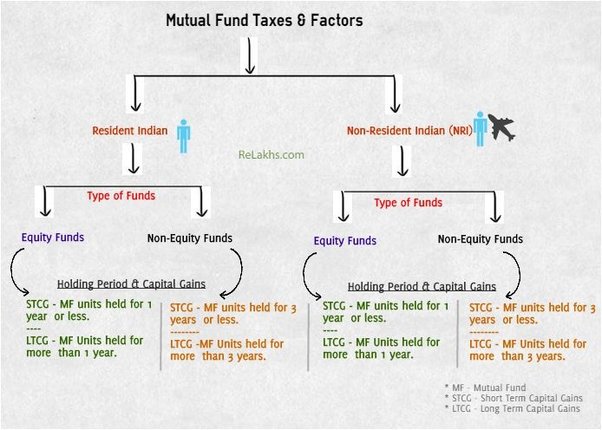

- Capital gains arising on the transfer or redemption of equity-oriented units held for a period of more than 12 months, immediately preceding the date of transfer, should be regarded as ‘long-term capital gains’.

- Capital gains arising on transfer or redemption of Units of schemes other than EOF shall be regarded as long-term capital gains, if such units are held for a period of more than 36 months immediately preceding the date of such transfer.

- As per section 112A of the Act, long-term capital gains on transfer of units of EOFs exceeding ₹ 100,000 shall be taxable @10% provided transfer of such units is subject to STT, without giving effect to first and second proviso to section 48 i.e., without taking benefit of foreign currency fluctuation and indexation benefit. Further, cost of acquisition to compute long-term capital gains is to be higher of (a) Actual cost of acquisition; and (b) Lower of (i) fair market value as on 31 January 2018; and (ii) full value of consideration received upon transfer.

- The lower rate @ 15% is optional for companies engaged in manufacturing business (set-up & registered on or after 1 October 2019) subject to fulfilment of certain conditions as provided in the section 115BAB.

- If a company decides to opt for the new taxation regime as per the Taxation Law Amendment Act, 2019, then tax shall be levied at the rate of 22%. i.e., the lower rate of 22% is optional and subject to fulfilment of certain conditions as provided in section 115BAA.

- Tax shall be levied @ 25%, if the total turnover or gross receipts of the financial year does not exceed ₹ 400 crores. Further, the domestic companies are subject to minimum alternate tax (except for those who opt for lower rate of tax of 22%/15%) not specified in above tax rates.

Securities Transaction Tax (STT) in respect of Units equity-oriented mutual fund Schemes:

- Various Categories of MF Schemes which fall under “Other than Equity Oriented Funds”:

- Liquid Funds /Overnight Funds / Money Market Funds / Income Funds (Debt Funds) / Gilt Funds

- Hybrid Fund (Equity exposure < 65%)

- Gold ETFs / Bond ETF / Liquid ETF

- Fund of Funds (Domestic) other than Fund of funds as defined under the “Equity Oriented Fund” definition under section 112A of the Act.

- Fund of Funds Investing Overseas

- Infrastructure Debt Funds

- OTHER TAX PROVISIONS

- Capital gains arising on Transfer of units upon consolidation of mutual fund schemes of two or more schemes of EOFs or two or more schemes of a Scheme other than EOF in accordance with SEBI (Mutual Funds) Regulations, 1996 is exempt from capital gains tax.

- Likewise, Capital gains arising on Transfer of units upon consolidation of Plans within a mutual fund scheme in accordance with SEBI (Mutual Funds) Regulations, 1996 is exempt from capital gains tax.

- Currently, switching units of mutual fund within the same scheme from Growth Plan to IDCW Plan (erstwhile Dividend Plan) and vice-versa is subject to capital gains tax.

- Creation of segregated portfolio: SEBI has permitted creation of segregated portfolio of debt and money market instruments by mutual fund schemes in certain situations. As per the said SEBI circular, all existing unit holders in the affected mutual fund scheme as on the date of the credit event shall be allotted equal number of units in the segregated portfolio as held in the main portfolio. As per sub-sections (2AG) and (2AH) to Section 49 of the Act, cost of acquisition of a unit or units in a segregated portfolio shall be the amount which bears to the cost of acquisition of a unit or units held by the assessee in the total portfolio in the same proportion as the net asset value of the asset transferred to the segregated portfolio bears to the net asset value of the total portfolio immediately before the segregation of portfolios. Further, the cost of acquisition of the original units held by the unit holder in the main portfolio shall be reduced by the amount as so arrived for the units of segregated portfolio.

- An Equity Oriented Mutual Fund has been defined in section 112A of the Act. As per the said definition, a fund of fund scheme structure shall be treated as an Equity Oriented Fund if:a minimum of ninety per cent of the total proceeds of such fund is invested in the units of such other fund; andsuch other fund also invests a minimum of ninety per cent of its total proceeds in the equity shares of domestic companies listed on a recognised stock exchange

Thus, if a fund invests in units of other funds and fulfils the aforementioned criteria, then it shall be regarded as Equity Oriented Fund. However, if the aforementioned conditions are not fulfilled, then the same shall be regarded as other than Equity Oriented Fund and subjected to the same tax treatment as applicable to a non-equity-oriented fund. - Bonus Stripping: As per Section 94(8), the loss due to sale of original units in the schemes, where bonus units are issued, will not be available for set off; if original units are: (A) bought within three months prior to the record date fixed for allotment of bonus units; and (B) sold within nine months after the record date fixed for allotment of bonus units. However, the amount of loss so ignored shall be deemed to be the cost of purchase or acquisition of such unsold bonus units held on the date of transfer of original units. The Finance Bill, 2022 has proposed to amend the provisions of the said sub-section such that it shall also be applicable to securities. Further, the definitions of the terms “unit” and “record date” are proposed to be expanded to also include the units of business trusts (i.e. Real Estate Investment Trusts [REITs]/ Infrastructure Investment Trusts [InvITs]) and units of Alternate Investment Funds in the ambit of the said section.

INCOME TAX RATES FOR INDIVIDUAL / HUF / AOP/ BOI – Old Tax Regime

INCOME TAX RATES FOR INDIVIDUAL / HUF – New Tax Regime

(a) In the case of a resident individual of the age of 60 years or more but less than 80 years, the basic exemption limit is INR 300,000.

(b) In the case of a resident individual of the age of 80 years or more, the basic exemption limit is INR 500,000.

(c) Plus, surcharge on income-tax, as applicable (Health and Education cess is applicable at the rate of 4% on income-tax and surcharge.)

(d) Rebate of upto ₹ 12,500 available for resident individuals whose total income does not exceed ₹ 500,000.

(e) Under section 115BAC, an option has been provided to pay tax at the above tax rates subject to the condition that certain exemptions/ losses/ deductions cannot be claimed. In case, the taxpayer intends to claim deductions / exemptions, the existing tax rates and slabs will continue to apply.

(f) Individuals having total income not exceeding ₹ 500,000 can avail rebate of lower of actual tax liability or ₹12,500.